To Author's Page

It’s hard to believe, but it’s true: “Pensions are safe!” was the slogan of the 1986 election campaign, coined by the Federal Minister of Labour at the time, Norbert Blüm. The older ones among us may still remember it.

And perhaps Norbert Blüm really was convinced that this was the case. However, things are looking very different in 2024. He wasn’t the only one to hold this mistaken view. Konrad Adenauer had also come to some false conclusions in the development and continuation of the old “Bismarckian” pension system: Almost 70 years ago, the former German Chancellor presumably stated that “people will always have children” in the upcoming pension reform of 1957. He was proved right for the next few years. In 1964, the highest number of children by far were born in Germany. But after that, things rapidly went downhill. The introduction of the pill took its toll, and a trend set in that has continued to this day. And there’s no change in sight. All the facts are clearly on the table. It’s not a sealed book or some sort of pension witchcraft, it’s simple maths. But you should know your basic multiplication tables when it comes to organising pensions for the future. Let’s start with the facts.

The decline in the birth rate

As the following chart shows, there has been a drastic decline in the birth rate over the past 60 years. While 1.36 million children were born in Germany in 1964, by 2023 this number had dropped to around 693,000 – a decline of more than 50 per cent. This has dramatic consequences. Unlike insurance companies, the pension system does not operate on a funded scheme, but on a contribution basis. This means that with their pension contributions, the current generations pay the money into the system that the older generation receives in pensions and lives on today. The state merely redirects the money from the contributors to the pensioners. But there are fewer and fewer contributors. People who do not exist are obviously also not on the labour market and do not pay contributions. The first observation is therefore that fewer people are being born so fewer will pay into the labour market in 25 or 30-years’ time. So far, so good, but what about the current and, above all, future pensioners?

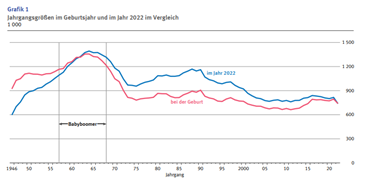

The baby boomers: At the peak of the demographic wave.

Source: Federal Statistical Office (destatis.de)

Another factor is the ageing population.

“While boys born in the Federal Republic of Germany around 1950 could expect to live for an average of 64.6 years, this figure had already risen to 78.5 years by 2020. In the same period, the life expectancy of girls rose from 68.5 years to 83.4 years.”

Source: Federal Statistical Office (destatis.de)

As a result, the average length of time a pension is drawn increases. As a logical consequence, the next factor also develops negatively. The cost of pensions will rise and there will be more pensioners drawing longer and possibly higher pensions. The interactive graphic illustrates the increase in the number of older people. More and more people are living longer. This is slowly throwing the system out of balance. If fewer people are paying into the system and the number of pensioners is increasing or drawing pensions for longer, this creates an imbalance.

In addition, socially and politically desired “gifts” are being made to groups of the population who have never paid into the pension system, or who have done so to a lesser extent. This includes mothers’ pensions to cover the time spent bringing up children.

All of these developments mean that the delta between income and expenditure of the German Pension Insurance Fund (Deutsche Rentenversicherung) is getting bigger and bigger. Since the money has to come from somewhere, the federal subsidy from tax revenue is increasing every year: In 1999, 25 years ago, this amounted to €42.53 billion; by 2024 it was already more than €100 billion from the federal budget – about one per cent of total government spending. This development cannot be financed in the long term.

So, in theory, there are a number of options. All of them are likely to be equally unpopular; politicians shy away from these measures because they threaten their own re-election, regardless of how right the decision is.

If we take the issue seriously, one decision is not enough. A mix of all measures would be the most effective approach. However, the quintessence of these findings is also different: Private pension provisions are necessary! The best way to achieve this is through successful and comprehensive customer advice, such as private investment advice or well thought-out estate planning. The earlier, the better. So that the fairytale does not turn into a nightmare and the awakening does not come as a nasty surprise to large sections of the population.

Frankfurt School gGmbH

Adickesallee 32-34

60322 Frankfurt am Main