Autorenprofil

Weight loss drugs, also known as GLP-1 drugs are now widely used in standard care, advancing diabetes and obesity treatment and promoting healthier lifestyles. Until 2032, estimated over 10 new market entries are expected to populate the German GLP-1 market, both from original pharmaceutical manufacturers and biosimilar producers, including Boehringer Ingelheim, Altimmune, Pfizer, Zentiva, Basics, and others. As a result, competition in the market will increase and pharmaceutical companies will have to defend their market position. Market forecasts expect a market growth in the following years. As of early 2026, the German GLP-1 market size is estimated at €2.3 billion. Obesity and type two diabetes are the two main medical conditions for a GLP-1 prescription. Although the prevalence for obesity remains relatively stable at around 21% (or 18 million adults) in Germany, health-conscious adults and lifestyle choices will drive the demand in the future.

Despite strong clinical outcomes, studies indicate that up to 65% of GLP-1 patients discontinue therapy within the first twelve months of treatment. In many cases, this attrition does not occur because the therapy is ineffective or the high treatment costs. Instead, patients frequently struggle with insufficient guidance between physician visits, uncertainty about treatment expectations and likely side effects they might encounter during therapy. Patients experience challenges especially in the early phase of treatment. The combination of GLP-1 dosage adjustment, physical side effects, and lack of structured reassurance often leads to anxiety and treatment interruption. Treatment discontinuation has a direct economic impact on pharmaceutical companies´ revenues due to decrease in sales of medication. In chronic disorders, treatment persistence is a key driver of value creation for pharma companies. Each additional month a patient remains on GLP-1 therapy increases both clinical outcomes and cumulative revenue for pharmaceutical companies. Consequently, improving treatment adherence represents an economic opportunity for pharmaceutical companies.

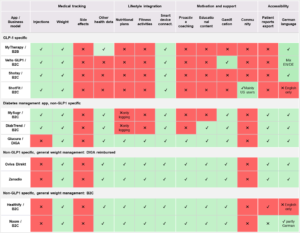

Our research, conducted as part of an EMBA thesis at Frankfurt School, suggests that medication-specific treatment companion apps can address this structural gap effectively (Table 1).

Table 1: mHealth apps available in Germany (1A, sources: App downloads and user manuals) and core features a tailored digital companion app should address (1B).

1A

1B

Apps provide structured patient support throughout the therapy journey, particularly during the most vulnerable early weeks of treatment. The application can combine medically validated treatment and symptom guidance, a personalized therapy journey aligned with dose progression, nutrition and lifestyle education that complements pharmacological treatment, moderated peer support, and a real-world data engine generating anonymized insights on patient engagement and persistence (GLPioneer*; see Figure 1).

Figure 1:GLPioneer* mock up user interface highlights five core functions.

The application can be branded for a pharma product and the user experience can be customised individually (e.g. treatment goals and medication plan).

The value created by drug specific applications extends across all key stakeholders (pharma, healthcare professionals and patients).

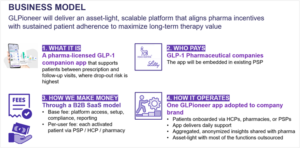

The business model around the mobile application can be deliberately structured to align with the commercial objectives of pharmaceutical companies. The platform is offered as a Business-to-Business Software-as-a-Service (SaaS) solution licensed to pharmaceutical companies and is well‑positioned to be integrated into existing patient support programs (PSPs). Each pharmaceutical partner receives a branded front-end interface for its patients, while the underlying data infrastructure operates as a shared white-label platform that allows scalable multi-client deployment.

This architecture enables the app provider to serve several pharmaceutical partners simultaneously while maintaining independent data environments for each company. The economic value of GLPioneer* is quantifiable (see Figure 2). Our model showed that even with a low adoption rate of 4% among GLP-1 patients and a 15% improvement in treatment persistence, pharmaceutical companies can increase their revenue significantly.

Figure2: Digital companion app business model at a glance.

The first of its kind digital companion tailored for a national healthcare market benefits from the early mover advantage and is likely to take center stage in a “winner-takes-all” digital solution market dynamic; which was observed on social media and career platforms in the past. In essence the first comprehensive digital companion for GLP-1 patients in Germany aimed at strengthening this ecosystem could be this early mover. A drug-specific digital companion app represents a commercially attractive business model and an attractive investment opportunity for early-stage investors. Overall, pharma competition on the GLP-1 market will increase due to new market entrants. Protecting revenue will define a major challenge for the industry.

Differentiation is likely to shift from molecule performance to treatment ecosystem quality (value-based approach), showcasing the viability of a companion app for commercial purposes. This is further reinforced by the recent economic reality of GLP-1 weight loss medication in the pharma sector. As a recent Financial Times article observes, the economics of weight-loss drugs continue to resemble those of traditional pharma. However, the established business model of weight loss drugs will not last much longer, due to considerable additional pricing competition from China and India (FT publishing on April 16th and 19th 2026). It can be expected that the ecosystem-driven value will become even more critical for long-term competitiveness.

We would like to thank Frankfurt School for providing the infrastructure and the network of expertise that made this work possible as part of the EMBA programme.

References:

Background and corresponding authors

This blog post is based on the findings of the EMBA master’s thesis “Business Plan for GLP-1 Receptor Agonist Treatment Companion App” (March 2026); corresponding authors: Dr. F. Haenisch, Dr. S. Kowalski, J. Leuschner, A. Matassova

Anna Matassova

Regional Head DACH Consumer Healthcare Norgine GmBH | Executive MBA, Frankfurt School of Finance & Management (Class of 2026)

Anna Matassova is a senior leader with 20+ years of experience in pharmaceutical and consumer healthcare, with a career spanning country leadership, global category management and regional business leadership.

Julia Leuschner

Julia Leuschner is a Senior Manager with 12+ years of experience in the pharmaceutical industry and consulting. She has guided organizations through complex transactions and transformations and brings deep expertise in strategy, valuation, and cross-functional leadership.

Dr. Sebastian Kowalski

Dr. Sebastian Kowalski is a Project Manager at Merck Electronics KGaA with over 9 years of experience in industrial R&D, specializing in semiconductor materials. He has expertise in process development and global operations, supported by a strong academic track record.

Frankfurt School gGmbH

Adickesallee 32-34

60322 Frankfurt am Main