To Author's Page

For decades, the banking industry has defined its “customer” as a person with a signature, a face, and a predictable 9-to-5 financial pulse. However, as we enter 2026, that definition is becoming dangerously obsolete. We are witnessing a fundamental shift where agentic AI is transitioning from a digital tool to an independent economic actor, and the capital flowing through these “clients” is going to explode.

The numbers tell a story of a market outrunning its regulators: the global agentic AI market is already valued at $7.55 billion as of 2025. It is projected to climb to $10.86 billion this year and skyrocket to approximately $199.05 billion by 2034. This represents a staggering compound annual growth rate (CAGR) of 43.84%.(1)

This hyper-growth is fueled by the rapid integration of AI across finance, transport, defense, and healthcare – industries increasingly relying on agents that can fully automate complex tasks without a single moment of human interaction. For financial service providers, the signal is clear: the most active users on your network tomorrow won’t be humans – they will be autonomous agents with the power to transact at a scale and speed that legacy banking rails were never designed to handle.

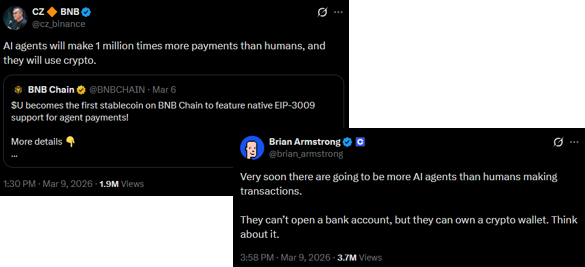

The significance of this development is echoed by industry leaders. This week, major signals emerged from the digital asset sector, with Coinbase CEO Brian Armstrong and Binance CEO (CZ)(2) both highlighting their preparation for a paradigm where machines, not just humans, are the customer.

Their remarks underscore a crucial trend: businesses are preparing for a world where AI agents open and manage their own digital wallets. For an AI agent, creating a stablecoin wallet and initiating transactions is vastly easier than navigating the legacy banking system. This efficiency advantage could rapidly make blockchain-based wallets the default financial tool for agentic AI.

This reality was cemented in March 2026, when Mastercard and Santander(3) successfully completed Europe’s first live end-to-end payment executed entirely by an AI agent. This milestone proves that the plumbing for autonomous commerce is being laid by the world’s largest financial institutions today.

Traditional financial institutions remain tethered to a human-centric model, where core processes like KYC, AML, and incident response are designed specifically to verify and monitor biological identities. This legacy framework, built on human behavioural patterns and manual oversight, is fundamentally incompatible with the high-velocity, autonomous nature of agentic AI clients.

Crucially, many of these processes remain heavily human-led, already resulting in significant backlogs and resource constraints for compliance teams today. Adapting this human-centric apparatus to accommodate machine-clients, which can operate at massive scale and high velocity, poses an enormous challenge.

This parallel is observed in other sectors, notably law enforcement. Where cybercrime units exist, they are often significantly under-resourced both in terms of technology and experienced human talent. This renders them largely unprepared for the speed and volume of cyber-enabled crime, a form of illegal activity that is quickly becoming, and partially already is, the dominant type of crime, especially as machine-augmented actors increase.

The traditional banking sector faces a similar dilemma in adapting. A stark warning was issued by EY(4), suggesting that banks risk losing the customer relationship if they do not facilitate wallet services for their clients. This statement, much like the preparations by Coinbase and Binance, signals a unifying vision of the future financial landscape.

“The Wallet is the Strategy… Who owns the wallet, who provides the wallet, will win the client relationship.”

– Mark Nichols (Principal, Capital Markets Strategy and Business Transformation, EY)

While the operational challenges are significant, the potential positive impact is equally profound. The inclusion of AI agents as active participants in the economy – an economy that is already largely digital – is poised to unlock entirely new markets and economic models. We are on the precipice of witnessing the emergence of true micro-economies. These would enable the pricing of services and utilities at a granular level previously impractical, even for values less than one EURO cent. Imagine an agent paying for individual search queries, discrete data points, or seconds of computational power.

For these hyper-efficient micro-transactions to flourish, the legacy financial infrastructure is inadequate. A new form of value exchange is required: one that is highly adaptable, efficient, and operates around the clock without manual intervention.

We predict this essential infrastructure will be enabled by stablecoins run on permissionless public distributed ledgers (blockchains). This combination provides the programmable, transparent, and scalable layer needed for seamless machine-to-machine commerce. The rise of agentic AI is evident. The race to define and serve the client of the future has already begun.

Deepen your expertise in the increasingly complex digital asset environment with Frankfurt School’s certified programme Digital Assets & Blockchain Expert (certified).

Frankfurt School gGmbH

Adickesallee 32-34

60322 Frankfurt am Main