To Author's Page

The future of auditing is significantly shaped by the deeper integration of agentic artificial intelligence (AI). The evolution of AI agents from mere supporters to autonomous actors capable of independently analyzing audit-relevant information and performing audit tasks is a pivotal development that is redefining the efficiency and quality of audits.

Today, AI models are applied in a variety of audit tasks such as journal entry testing [1], sample selection [2], or the review of financial reports [3]. However, a fundamental advancement in recent years denotes the development of agentic AI systems. These systems go beyond the simple application of AI models and exhibit the capability of independently planning audit processes, making decisions, and flexibly adapting to new challenges.

Biological models inspire the principle of AI agents: they perceive their environment, process information, and respond accordingly. Like how humans use their sensory organs to detect stimuli and react, AI agents rely on specialized models such as GPT-4[1], Gemini[2], or Llama[3]. Such AI models serve as the agent’s brain that transforms perceptions into targeted actions, allowing the agent to act autonomously and flexibly. Through continuous learning and adaptation, they can dynamically interpret their surroundings and respond to new challenges.

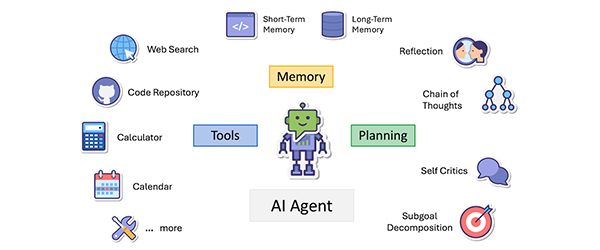

Figure 1: Overview of an AI agent’s capabilities—planning, memory, and tools—working together to enable dynamic and autonomous actions [9].

One of the strengths of AI agents lies in their ability to collaborate with human auditors. This is achieved through a variety of capabilities that allow them to engage in audit processes flexibly and situationally [6]:

The interplay of planning, memory, and tools enables the integration of agentic workflows [7, 8] into auditing. Additionally, complex audit processes can be carried out by collaborating multiple specialized and autonomous AI agents.

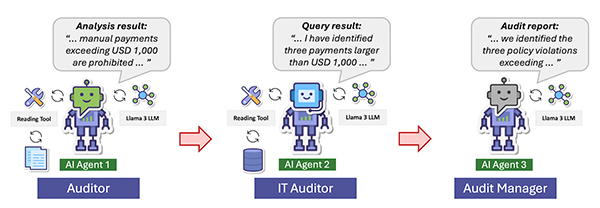

Figure 2: Auditing journal entries within an Enterprise Resource Planning (ERP) system through the application of agentic artificial intelligence.

The audit of journal entries (International Standard on Auditing 240) demonstrates how agentic AI can be applied in the audit process. The agentic audit process involves three AI agents, each responsible for specific tasks, working collaboratively to perform the audit:

During the audit execution, the intermediate results generated by the specialized AI agents build on each other, culminating in the final audit report.

AI agents, autonomously performing audit tasks and processes, can shape the next chapter of artificial intelligence and intelligent co-pilots in auditing. The future of auditing lies in the symbiotic collaboration between humans and agentic AI systems. At the same time, this development underscores the urgent need for new competencies in AI governance. Auditors will increasingly face the challenge of verifying the correctness of the results produced by AI agents. The Certified Audit Data Scientist certificate program addresses this innovative audit paradigm and imparts knowledge of advanced audit procedures. Agentic AI holds the potential to make audit processes more efficient, scalable, and of higher quality.

Aus Daten lernen: Verfahren Künstlicher Intelligenz in der Wirtschaftsprüfung

Prüfen mit intelligenten Co-Piloten: Generative Künstliche Intelligenz im Audit

Artificial Intelligence Agentic Auditing

Certified Audit Data Scientist – Neue Perspektiven für Ihr Prüfungsvorgehen

This blog post presents an excerpt from the following work, co-authored by the author: “Artificial Intelligence Agentic Auditing,” Schreyer, M., Gu, H., Moffitt, K., and Vasarhelyi, M. A. (Social Science Research Network, 2024).

Bibliography:

[1] Schreyer, M., Baumgartner, M., Ruud, T. F., Borth, D. (2022) Artificial Intelligence in Internal Audit as a Contribution to Effective Governance – Deep-Learning Enabled Detection of Anomalies in Financial Accounting Data. EXPERTSuisse, Expert Focus, pp. 45-50.

[2] Schreyer, M., Gierbl, A. S., Ruud, T. F., Borth, D. (2022) Artificial Intelligence Enabled Audit Sampling-Learning to Draw Representative and Interpretable Audit Samples from Large-Scale Journal Entry Data, EXPERTSuisse, Expert Focus, pp. 106-112.

[3] Deußer, T., Leonhard, D., Hillebrand, L., Berger, A., Khaled, M., Heiden, S., … & Sifa, R. (2023). Uncovering Inconsistencies and Contradictions in Financial Reports using Large Language Models. IEEE International Conference on Big Data, pp. 2814-2822.

[4] Russell, S. J., & Norvig, P. (2016). Artificial Intelligence: A Modern Approach. Pearson.

[5] Kolt, N. (2024). Governing AI Agents. SSRN (Abstract ID: 477295)

[6] Weng, L. (2023). LLM Powered Autonomous Agents (https://lilianweng.github.io)

[7] Ng, A. (2023). AI Agentic Workflows and Their Potential for Driving AI Progress [Video]. YouTube. https://www.youtube.com/watch?v=q1XFm21I-VQ

[8] Ng, A. (2023). What’s next for AI agentic workflows [Video]. YouTube. https://www.youtube.com/watch?v=sal78ACtGTc

[9] Schreyer, M., Gu, H., Moffitt, K., und Vasarhelyi, M. A. (2024) Artificial Intelligence Agentic Auditing, Social Science Research Network (SSRN).

Frankfurt School gGmbH

Adickesallee 32-34

60322 Frankfurt am Main