To Author's Page

Auditors increasingly employ artificial intelligence (AI) models to gain insights into complex audit-relevant matters. These AI models have the ability to store knowledge generated by various entities that are subject to an audit. Once learned, AI models can assist auditors in a range of audit procedures. [1],[2] Lately, AI models have been progressively used for tasks such as audit sampling, [3] journal entry testing, [4] and auditing disclosures in financial notes. [5]

Auditors acquire collective expertise through various audit mandates and procedures in their professional careers. This diversity of experiences enables them to advance and specialise their skills. At the same time, such a learning setting raises the question: How can collective experiences be realised in AI model learning?

In parallel, auditors are exposed to confidential and personal information. Consequently, AI model learning must comply with data protection, security, and confidentiality regulations. Keeping sensitive organisational data private while accumulating knowledge from various entities is, therefore, of paramount importance. Federated-learning enables multiple entities, e.g., audit clients or organisational units, to train advanced AI models collaboratively. The collaborators proprietary data, processed in the collective model training, is not exchanged among the participating entities.

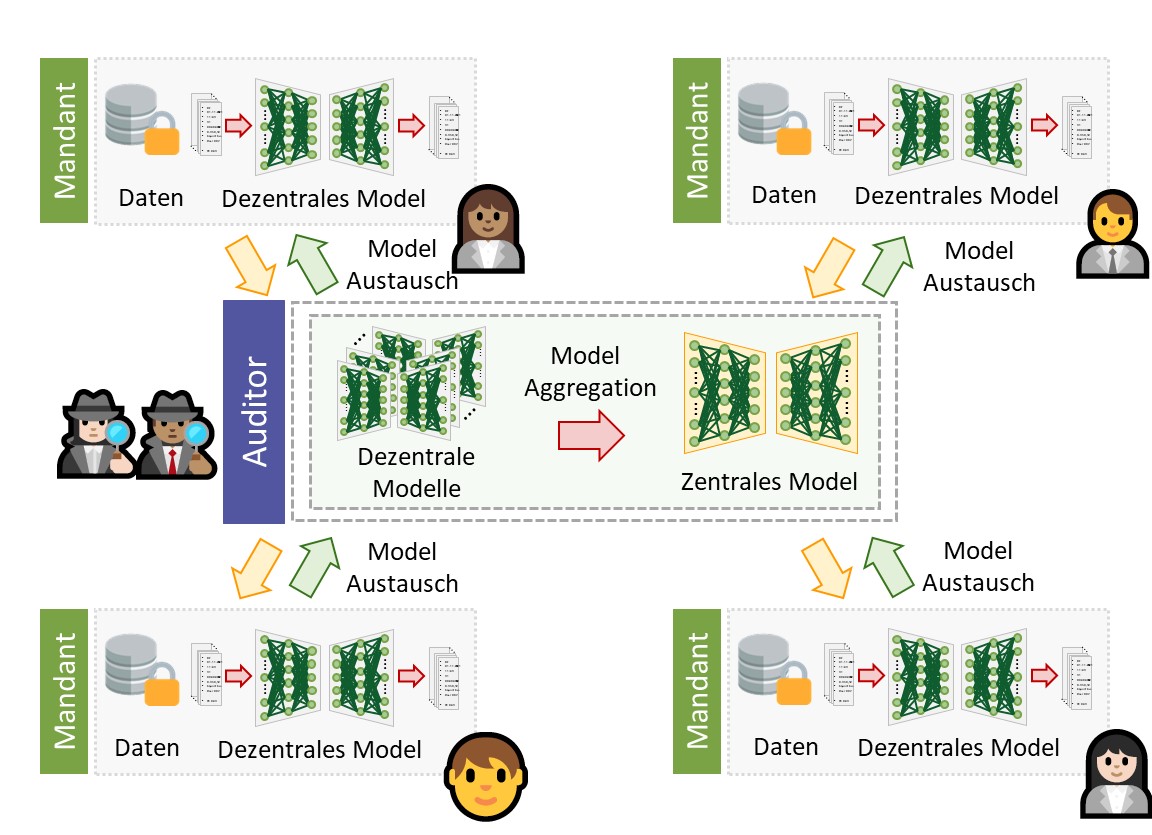

Federated-learning[6] distinguishes between central and decentralised AI models. A central AI model is learned through the collaboration of several decentralised entities. Each entity trains a local, decentralised AI model. Once these individual learning processes are completed, the models are merged into a central model. In financial auditing, a federated-learning process can be implemented through the following six steps: [7]

Steps 2-5 of the federated-learning process are iteratively repeated to continuously improve the central AI model. As the learning progresses, the central AI model increasingly integrates the collective intelligence of the participating entities. Once the learning is completed, the central AI model is accessible for beneficial use by all collaborating entities.

Figure: Illustration of a federated-learning process to learn a central AI model in financial auditing, utilising proprietary accounting data from various collaborating audit clients.[8]

Federated-learning enables the optimisation of AI models while complying with data privacy and confidentiality regulations. It enables auditors to leverage diverse data sources to learn models for complex audit procedures.[9] A study by Hoitash et al. [10] demonstrated that incorporating peer-client data in AI model training results in improved AI model predictions.

Internal auditors can employ federated-learning to train advanced AI models at the organisational level, helping to mitigate risks and enhance audit quality. Additionally, external auditors can use federated-learning to train AI models across various sectors, thereby utilising collective intelligence to improve audit efficiency.

AI models that draw on the paradigm of collective intelligence to enhance their capabilities have the potential to redefine the future of AI co-piloted auditing.[11] The Frankfurt School’s Certified Audit Data Scientist program incorporates these innovative learning paradigms and imparts knowledge of advanced audit procedures.

———————————————————————————————————————————–

This blog post is an excerpt from the following article published by the author along with co-authors: A Sum Greater than its Parts: Collective Artificial Intelligence in Auditing – Advancing Audit Models through Federated-Learning Without Sharing Proprietary Data, Schreyer, M., Borth, D., Flemming, T. F., and Vasarhelyi, M. A. (EXPERTSuisse, Expert Focus, April 2024, pp. 180-186).

———————————————————————————————————————————–

[1] Gu, H., Schreyer, M., Moffitt, K., & Vasarhelyi, M. A. (2023). Artificial Intelligence Co-Piloted Auditing. SSRN. https://doi.org/10.2139/ssrn.4444763

[2] Eulerich, M., & Wood, D. A. (2023). A Demonstration of How ChatGPT Can be Used in the Internal Auditing Process. SSRN. https://doi.org/10.2139/ssrn.4519583

[3] Schreyer, M., Gierbl, A. S., Ruud, F., & Borth, D. (2022). Stichprobenauswahl durch die Anwendung von Künstlicher Intelligenz-Lernen repräsentativer Stichproben aus Journalbuchungen in der Prüfungspraxis. Expert Focus, (02), 10-18.

[4] Schreyer, M., Baumgartner, M., Ruud, F., & Borth, D. (2022). Künstliche Intelligenz im Internal Audit als Beitrag zur effektiven Governance-Deep-Learning-basierte Detektion von Buchungsanomalien in der Revisionspraxis. Expert Focus, (01), 39-44.

[5] Ramamurthy, R., Pielka, M., Stenzel, R., Bauckhage, C., Sifa, R., Khameneh, T. D., Warning, U., Kliem, B., & Loitz, R. (2021, August). Alibert: Improved Automated List Inspection (ALI) with BERT. In Proceedings of the 21st ACM Symposium on Document Engineering (pp. 1-4).

[6] Konečný, J., McMahan, H. B., Yu, F. X., Richtárik, P., Suresh, A. T., & Bacon, D. (2016). Federated learning: Strategies for improving communication efficiency. arXiv preprint arXiv:1610.05492.

[7] Kairouz, P., McMahan, H. B., Avent, B., Bellet, A., Bennis, M., Bhagoji, A. N., … & Zhao, S. (2021). Advances and open problems in federated learning. Foundations and Trends in Machine Learning, 14(1–2), 1-210.

[8] Schreyer, M., Sattarov, T., & Borth, D. (2022, November). Federated and privacy-preserving learning of accounting data in financial statement audits. In Proceedings of the Third ACM International Conference on AI in Finance (pp. 105-113).

[9] Seidenstein, T., Marten, K. U., Donaldson, G., Föhr, T. L., Reichelt, V., & Jakoby, L. B. (2024). Innovation in audit and assurance: A global study of disruptive technologies. Journal of Emerging Technologies in Accounting, 21(1), 129-146.

[10] Hoitash, R., Kogan, A., & Vasarhelyi, M. A. (2006). Peer-based approach for analytical procedures. Auditing: A Journal of Practice & Theory, 25(2), 53-84.

[11] Please, add link to previous Frankfurt School blog post: Frankfurt School Blog | Auditing with intelligent co-pilots: Generative Artificial Intelligence in Audit (frankfurt-school.de)

Frankfurt School gGmbH

Adickesallee 32-34

60322 Frankfurt am Main