To Author's Page

“The fossil fuel industry is not the enemy – it is the emissions,” declared Mia Mottley, Prime Minister of Barbados.

If that’s the case, then every organisation must manage their emissions as relentlessly as cashflows. Yet emissions accounting is prohibitively complicated and expensive – only done by a handful of companies. It also lacks the rigour and auditability of financial accounting. The resulting approximations may help companies or governments know where start – but they’re not enough to decarbonise our complex market economy.

Consider a haulage company. They know that their biggest emissions are from their diesel burning trucks. The quick-win solution seems obvious – switch to a zero-emissions fleet.

After deciding to go electric, the remaining biggest emissions are embodied in the vehicles, embedded deep in their supply chains. To make an informed decision about which trucks to buy, the company needs reliable product carbon footprint (PCF) data, presented alongside the price at the point of purchase.

Globally, roughly 23,000 companies disclose their emissions according to the Greenhouse Gas (GHG) Protocol – the de facto standard. But that equates to merely 0.008% of the world’s 300 million businesses. It doesn’t even get close to the potential data requirements. In Europe alone, there are over 150 billion non-cash payments made every year. With every one of these, the buyer is aware of price – but rarely the emissions.

The solution is (theoretically) simple – to include emissions data in financial accounting systems so that the PCF data can be displayed on price tags and invoices.

This requires a paradigm shift in how we think about emissions data. It’s already possible to price products in multiple currencies for sale in different countries – so it’s not that hard to add another “currency” denominated in CO2e for the emissions cost.

Counterintuitively, reframing the challenge around this need for granular data also makes it easier to solve the problem of corporate disclosure – after all, as I’m reminded by Hilary Eastman, corporate accounts are the summation of a company’s granular transactions.

When emissions data are in the financial accounting systems of companies, then they can also be submitted together with periodic tax returns, like VAT. Imagine, just “one click” for submitting both tax returns and emissions disclosure – radically simple and painless!

The reason is elegantly summarised by Dr Ulf von Kalckreuth, Principal Economist-Statistician at the Deutsche Bundesbank (German central bank). He explains that the “GHG Protocol Standards were developed around the turn of the millennium for a world in which only few and isolated companies decided to give an account of their carbon emissions – voluntarily. At the time, there was no use in pointing to the accounting work of others as a prime source of information.”

In that context, the GHG Protocol was right to implement a business management logic that amplifies emissions hotspots and highlights feedback loops, both upstream and downstream. What financial accountants and macroeconomic statisticians nowadays consider multiple counting, the GHG Protocol frames as an essential way of revealing which companies, industries, and supply chain configurations can have the biggest effect in reducing systemic emissions.

But now we need a more rigorous data science approach to satisfy more demanding requirements. Regulations, like the EU’s Carbon Border Adjustment Mechanism (CBAM), require robust data that can withstand the scrutiny of international trade litigation.

We can learn lessons from photography, when it transitioned from chemical film to digital processing.

The fundamental principles of photography did not change with the advent of digital technologies, neither is climate science changing – but operationally, the way to do emissions accounting is changing (and must change). Fortunately – like with all truly disruptive innovations – the data science approach makes emissions accounting easier, faster, cheaper, and more accurate.

This longer technical article explains how: The False Conflict Holding Back Emissions Accounting – And the Need for Harmony of Standards and Collegiate Collaboration

Paradoxically, the lingua franca of the GHG Protocol is subconsciously blocking the change.

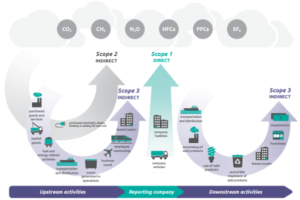

The terms “scope 1”, “scope 2”, and “scope 3” trap people in a mental model that hinders a data science way of thinking. The problem is that the “scopes” essentially differentiate emissions based on the convenience of obtaining data, they are not classifications based on fundamental data characteristics.

This matters because it’s suppressing the era of radical simplicity.

Just like John Elkington did a “product recall” when the triple bottom line concept he founded was no longer fit for purpose, the GHG Protocol ought to recall the “scopes”.

Even in the totemic image (above) from the GHG Protocol, the labels beneath the “scopes” delineate the three fundamental data categories:

If these three classifications appear self-evident and more intuitive than “scopes”, then you already think like a data scientist.

Frankfurt School gGmbH

Adickesallee 32-34

60322 Frankfurt am Main